Hong Kong Dollar’s Volatility Fuels Talk on How FX Peg May Shift

A fresh about the sustainability of Hong Kong’s decades-long currency peg has analysts ruminating on what might eventually replace it.

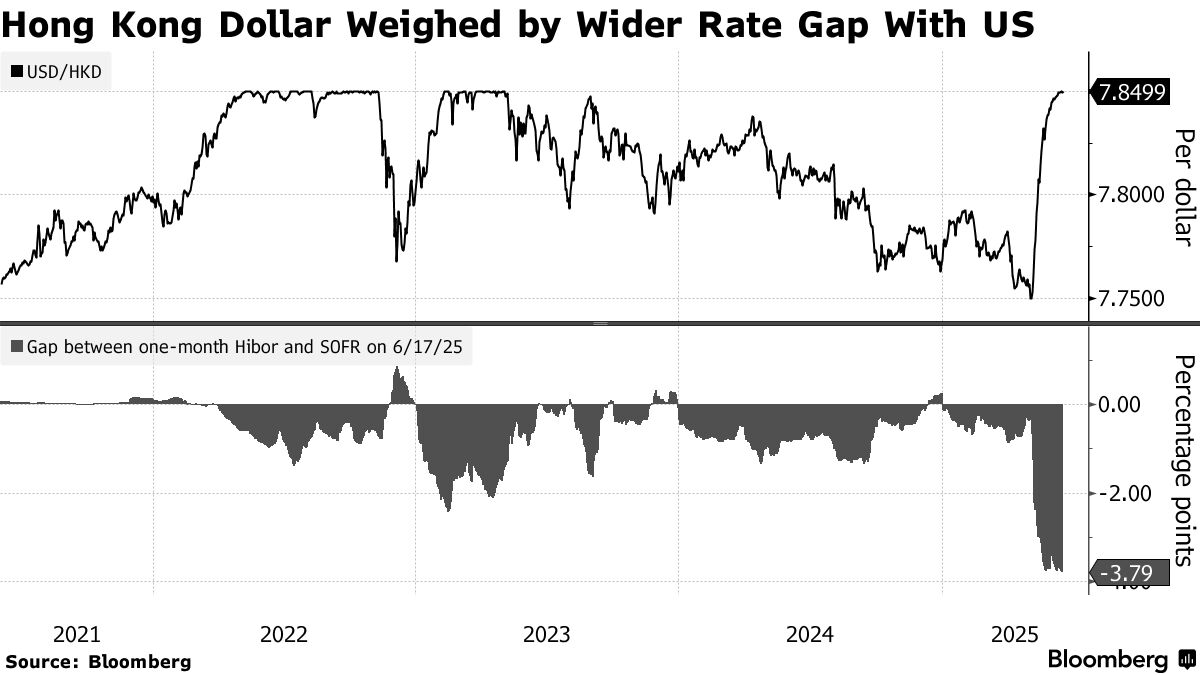

It’s an issue that’s gaining traction after intervention by authorities to defend the peg set off a bout of volatility in the in recent weeks. The currency continues to hover near the weak end of its trading band following a slide in the city’s interest rates to a three-year low.

The volatility that has buffeted the Hong Kong dollar highlights the dilemma which is confronting authorities as they seek to preserve a fixed exchange rate that’s integral to the city’s appeal as a financial hub. If the Hong Kong Monetary Authority intervenes aggressively to boost the local currency, there’s a risk that it may hurt consumption and undermine a nascent recovery in the property market.

To be clear, there’s no talk that Hong Kong will abandon its current practice of fixing the local dollar at 7.75–7.85 to the greenback anytime soon. But the rigidity of the pegged exchange rate and the US currency’s weakness are sharpening the focus on the possible alternatives that authorities may adopt in its place, if a shift ever occurs.

“We continue to see strong resolve and capability from local authorities to maintain the linked exchange rate, even at the cost of economic pain,” said Cindy Keung , an economist at OCBC Bank. “Any undesirable consequences due to the rigidity of currency board system should be managed by macro-prudential tools and fiscal measures.”

Here are some of the potential alternatives being discussed by analysts:

The most viable option is to peg the Hong Kong dollar to a basket of currencies to diversify the city’s risks as a global trading hub, according to DBS Bank, Union Bancaire Privee and Oversea-Chinese Banking Corp.

This system provides stability, “while reducing the pro-cyclical headwinds associated with the peg to the US dollar, as the business cycle becomes increasingly correlated with that of mainland China,” said Carlos Casanova , senior Asia economist at UBP in Hong Kong.

The downside is that the system may be less transparent and more complex for authorities to manage.

Some market watchers say it makes sense to peg the Hong Kong dollar to the yuan given the city’s deepening economic ties with China. Such a regime would reduce exchange rate volatility between Hong Kong and the mainland, and lower transaction costs for companies given the city’s growing trade and investments flows in and out of China. It would also minimize the Hong Kong dollar’s exposure to the greenback’s volatility, simplify cross-border transactions and facilitate the internationalization of the yuan.

“This is an ideal arrangement, given that the Hong Kong economy has seen greater integration with the mainland,” Societe Generale SA analysts Kiyong Seong and Michelle Lam wrote in a note. “But this will not be feasible until the RMB has achieved full capital account convertibility, which is unlikely to happen in the near future.”

This option would allow the city to maintain its current monetary policy framework, while ensuring greater flexibility to absorb economic shocks. The city last expanded the trading band in 2005, when it widened the range to 7.75 to 7.85 per dollar from 7.8.

A larger trading range would enable the HKMA to tolerate bigger fluctuations in the local dollar and reduce its need to intervene. It may also deter speculators from betting against the Hong Kong dollar as a wider trading band would expose the exchange rate to more uncertainties.

But some warn that it may encourage traders to wager on future shifts in the pegged exchange rate. “Once the range is widened, the market may continue speculating on the HKMA’s next move, which could erode confidence in the peg,” said Carie Li , global market strategist at DBS Bank.

If the HKMA adopts a free float, this will allow market forces to dictate the Hong Kong dollar’s moves and enable the currency to reflect the city’s economic fundamentals. But it will subject the local currency to massive swings during periods of volatility in global markets and potentially damp Hong Kong’s appeal as a global financial center.

Bearing in mind that the peg was adopted in 1983 to arrest the plunge in the exchange rate amid talk about the handover of the British colony to China, it seems unlikely that policymakers would choose to go for a free float.

A system that’s linked to gold would insulate the Hong Kong dollar from the swings in other currencies and reduce its dependence on the US and other countries at a time of rising geopolitical risks. The upward trajectory in the precious metal’s price may add to the appeal of such an option.

On the flip side, DBS notes that the gold market is not as liquid as Treasuries while UBP says such a link would expose Hong Kong’s financial sector to fluctuations in prices of the commodity.