Hong Kong Dollar Carry Trade Is ‘Over’ on Soaring Funding Costs

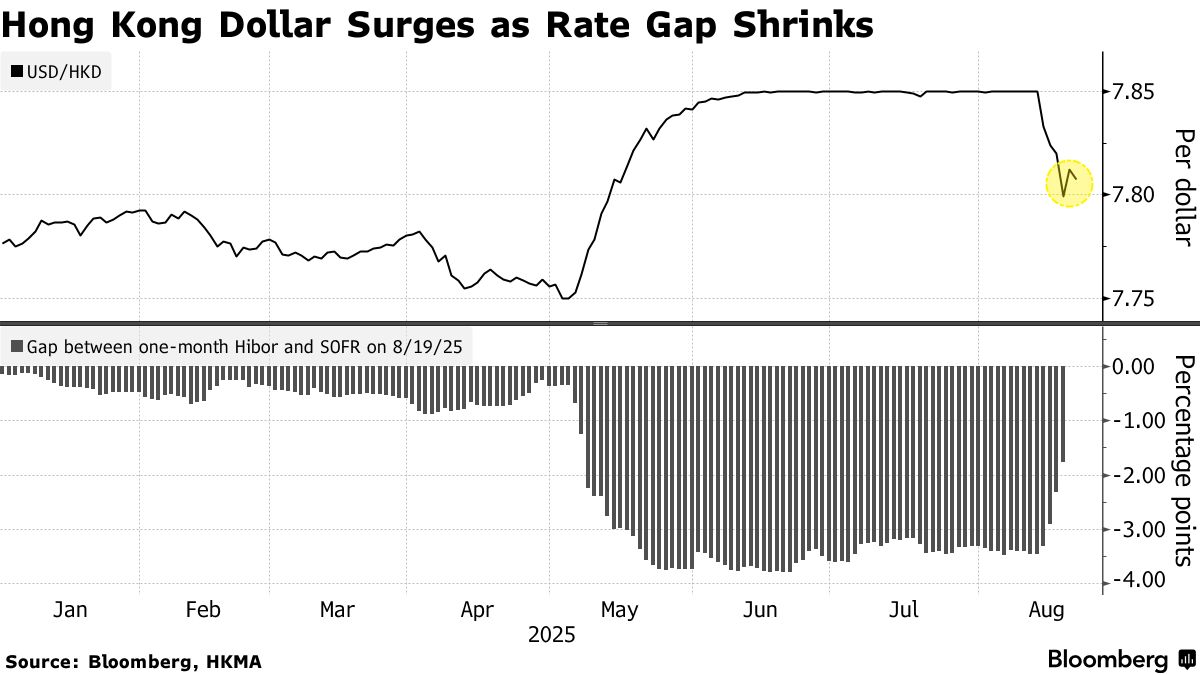

A surge in Hong Kong interest rates is upending what was the world’s earlier this year, after local authorities engineered a cash squeeze to ease pressure on the city’s decades-old currency peg.

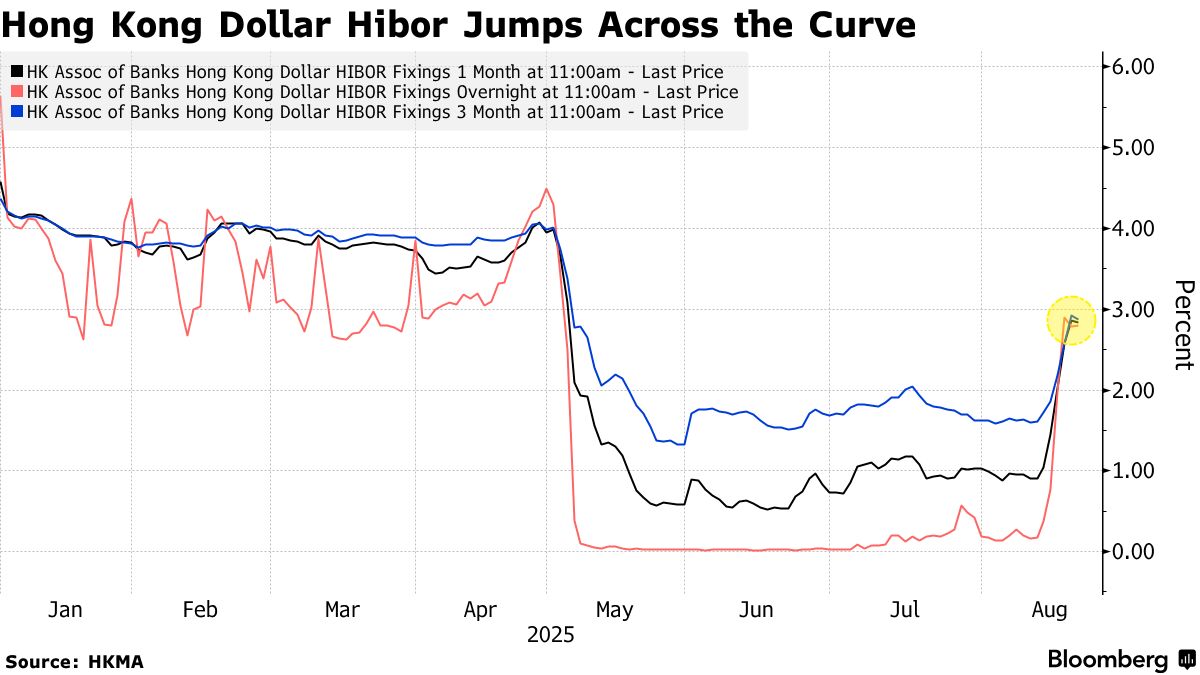

The strategy of borrowing Hong Kong’s currency cheaply to invest in the higher-yielding US dollar has become less profitable after the benchmark one-month Hong Kong Interbank Offered Rate, or Hibor, roughly in the five sessions before Thursday.

Around 30% of hedge funds’ $42 billion worth of long US dollar positions versus Hong Kong’s currency were unwound due to market moves and intervention by the city’s de facto central bank, Barclays Bank’s strategists estimated in a note dated Tuesday. The greenback’s further weakness and continued equities inflows into the financial hub may exacerbate the trend, they added.

The spike in funding costs was itself the result of the Hong Kong Monetary Authority’s efforts to use tighter liquidity to its currency, which had in recent months been testing the weak end of its HK$7.75-HK$7.85 official trading band against the greenback. Meanwhile, strong inflows into the city’s and a nascent recovery in loan demand will likely keep local interest rates elevated for now.

“The carry trade using the Hong Kong dollar as a funding currency is over for now — it was fun while it lasted,” said Khoon Goh , head of Asia research at Australia & New Zealand Banking Group. “It is no longer an attractive funder, which should see the currency maintain near the middle of the band.”

The HKMA’s liquidity withdrawals, which have taken place more than 10 times since late June, have caused an indicator tracking the size of interbank liquidity to drop by some 70% over the last two months.

This is a sharp reversal from just a few months ago, when a record-wide interest rate gap between the US and Hong Kong demand for the carry trade. Ironically, the Hibor’s slump at that time was the direct outcome of the HKMA’s liquidity injection to prevent a weaker US dollar from sending the city’s currency beyond the strong end of the narrow trading band.

The latest spike in Hibor has more than halved its discount to its US equivalent since a peak in June to about 150 basis points, significantly reducing the returns from the carry trade. Meanwhile, the Hong Kong dollar rose earlier this week to its strongest level since May against the greenback and beyond the mid-point of its trading band.

The Hang Seng Index has risen 25% this year, making it one of the world’s top-performing major stock gauges. Key to its success has been hefty purchases by mainland Chinese investors, who poured in ($4.6 billion) last Friday.

“Investors now have more options to deploy capital into assets with potentially higher returns,” said Gary Ng , senior economist at Natixis. “The incentive to initiate new carry trades is no longer as strong as before.”

Also of help is local loan demand that has picked up following a post-pandemic slowdown. The latest data show that the city’s loan-to-deposit ratio rose the most since early 2023 in June.

“Overall positive Hong Kong equity sentiment and inflows should result in a stabilization of front-end rates after the recent squeeze,” Nomura strategists led by Craig Chan wrote in a note. “However, the long end still has upside potential over the medium term, if loan demand gradually recovers.”