Emerging-Market FX Swings Top Developed Peers After Record Lull

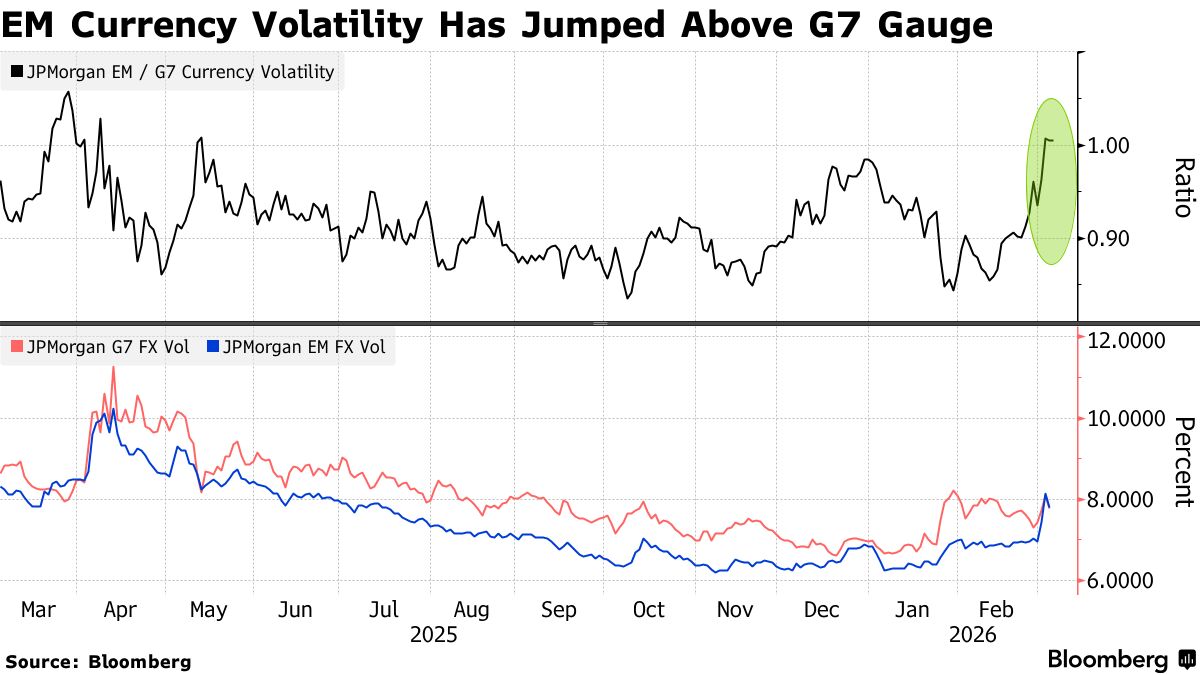

Emerging-market currency volatility has surged above that of developed-market peers this week for the first time since May, breaking a stretch that was the longest on record.

JPMorgan’s EM volatility index rose above a similar Group-of-Seven gauge on Tuesday after 209 days below it — the in data going back to 2000. That happened as surged to the highest since July 2024 this week due to the Iran war, and South Korea’s index suffered a record drop on Wednesday.

“EM FX volatility has been impacted by escalating Middle East tensions, and from the second-order effect after the volatile performance from Asian equity bourses such as the Kospi,” said Mingze Wu , a currency trader at StoneX Financial Pte. in Singapore. “EM FX volatility relative to DM should ease once Middle East tensions cool down.”

Nearly all EM currencies have fallen against the dollar this week, swept along by the risk-off sentiment and surge in oil prices. But that may not change the wherein strong commodity prices and robust capital inflows have supported demand for EM assets and helped make carry trades attractive, while the greenback has been weakening.

“Oil is the key driver for weaker EM currencies and therefore recent higher volatility too, ”said Wee Khoon Chong , a strategist at BNY in Hong Kong. “A de-escalation in Middle East tensions could draw back carry demand for higher-yielding EM currencies, and therefore driving EM FX volatility lower.”

On Tuesday, the won suffered its largest single-day loss on a closing basis since 2009, as investors warned of the risk of forced deleveraging and liquidations, which might lead to an indiscriminate selloff of assets to reduce risk.

Oil prices may continue to play a role in the performance of EM currencies in a different way as well, with a difference between those of crude importers and exporters, according to Barclays Bank Plc and Goldman Sachs Group Inc. Korea’s won , the Singapore dollar and India’s rupee are more vulnerable to supply shocks since they’re net oil importers, Barclays strategists wrote .

“Once investor positioning is more neutral,” there’s potential for a quicker recovery from currencies of Latin American oil exporters such as the Brazilian real and Colombian peso, Goldman strategists including Kamakshya Trivedi wrote in a note on Tuesday.

Click here for BI’s comprehensive global research on the Iran War.