Euro Attracts Bullish Options Buyers as Currency Goes Off Script

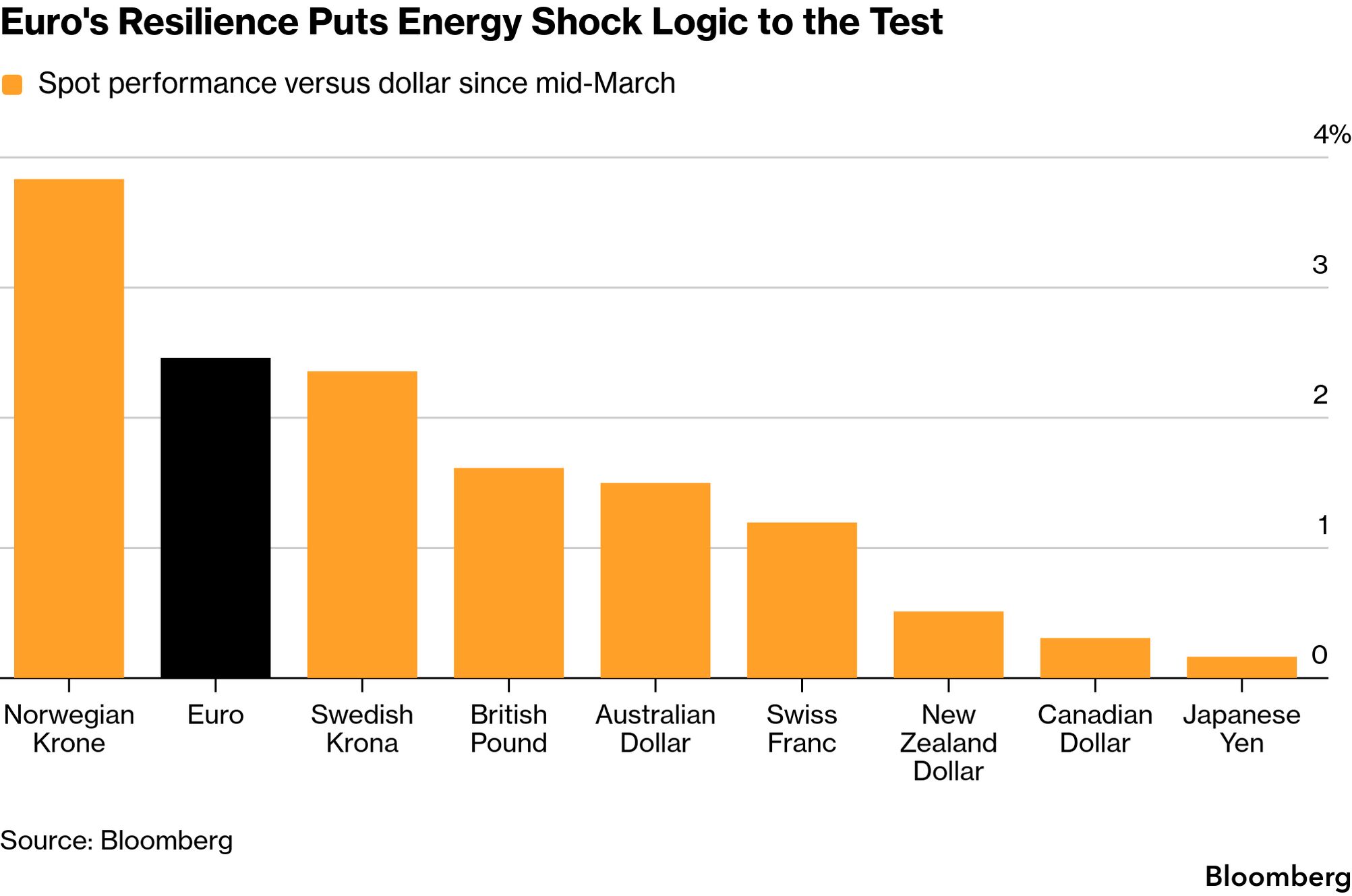

The euro is the second-best G-10 performer against the dollar over the past month, defying expectations that the energy shock caused by the Middle East war would hit Europe’s economy and drag the currency lower.

More than seven weeks into the war, the euro is trading near $1.18, roughly the same level as before the US and Israel launched strikes against Iran. Looking ahead, options traders say that a mix of steady prices and low volatility is creating even more demand for bullish bets.

The euro has, essentially, gone off script. Energy prices did spike in Europe, which relies on imported gas to power factories and heat homes. The prospects for peace are unclear, and the Strait of Hormuz remains effectively blocked. Yet the euro has largely stabilized, with hedging costs returning to pre-war levels by early April, even as sterling and the yen still reflected elevated risk.

“The conflict is still not resolved and we are back down already — is the market bored with it?” asked Andreas Koenig , global head of FX at Amundi SA, which manages about $2.6 trillion in assets.

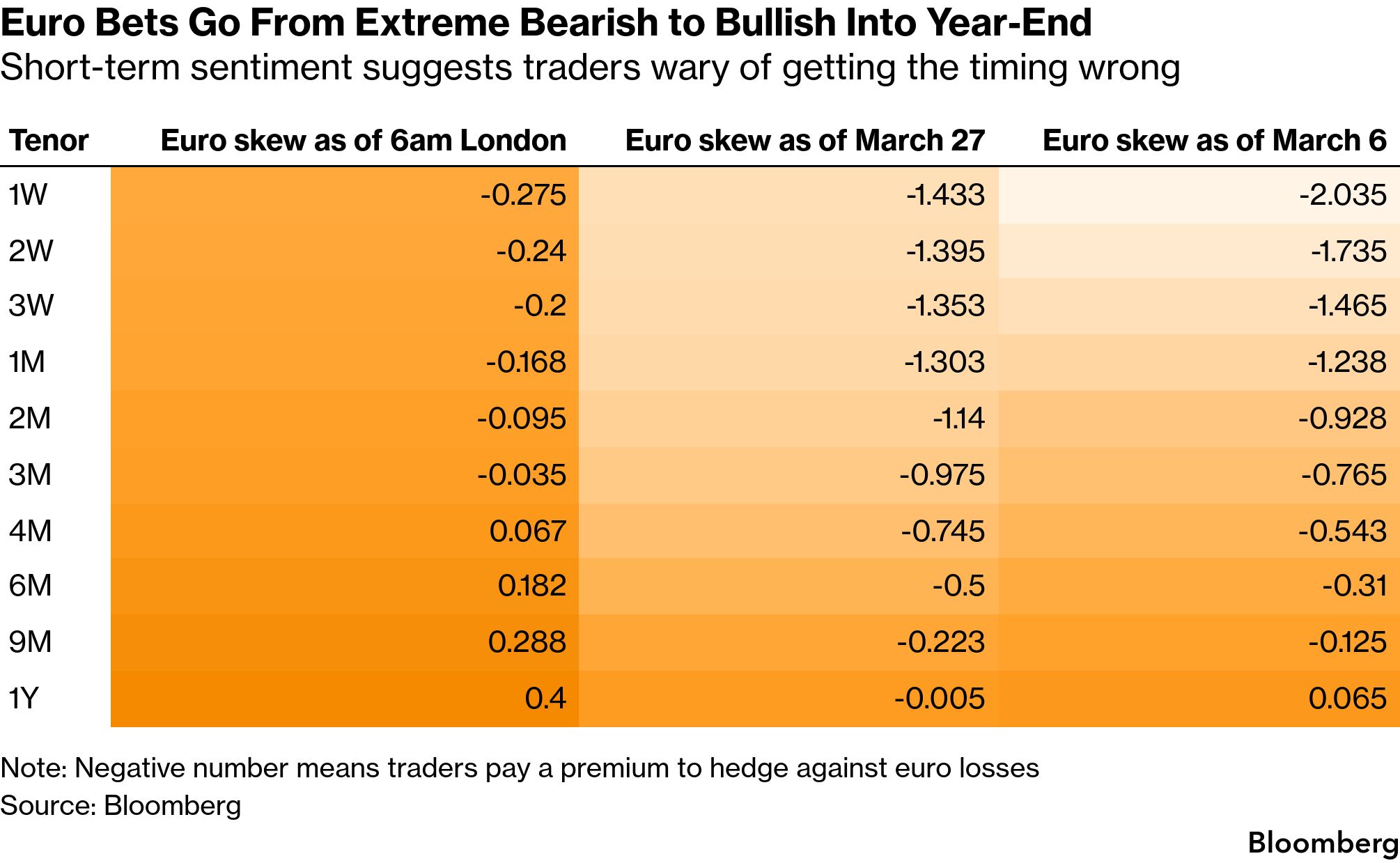

Hedging costs over the next month remain subdued, with implied volatility near 6%, short of this year’s highs above 9% and below the longer-term average. At the same time, traders are bullish on the currency’s prospects. That can be seen in the price action on one-year risk reversals, which gauge how expensive it is to buy versus sell a currency in the options market.

It’s unclear why the euro has performed so well following an initial dip in the opening phase of the war, but the dynamic has opened the door for directional trades that are attracting both hedge funds and longer-term institutional investors.

Amundi has been buying euro options that only kick in if the currency dips to $1.16. The idea is two-fold: if the conflict escalates and the euro weakens, the option takes effect; if tensions later ease, a broader view that the dollar will gradually slide comes into play.

“My view is still unchanged — the dollar will slowly go lower,” Koenig said during an interview last week.

Similar demand is showing up elsewhere. Interest in options that will pay out if the euro strengthens to $1.20 has re-emerged, while some hedge funds are looking at call spreads and other bullish structures, according to traders familiar with the transactions who asked not to be identified because they aren’t authorized to speak publicly. The common thread is limited downside as the market thinks the dollar will weaken against the euro but wants protection against getting the timing wrong.

Flow data support the thesis. Data from the Depository Trust & Clearing Corporation show dollar-bullish positioning in EUR/USD fell for seven consecutive weeks through last week. With the European Central Bank expected to keep borrowing costs steady at its next meeting, near-term rate drivers are limited, leaving the pair more sensitive to geopolitical headlines.

That leaves the Hormuz flare-up over the weekend as the first real test of whether the trade holds.

The euro “has remained surprisingly steady near $1.18 despite the rapidly shifting situation in the Middle East,” said Kirstine Kundby-Nielsen , a senior FX analyst at Danske Bank. “While a prolonging conflict remains a key downside risk for the cross, moderating energy prices have at least partially eased the negative terms-of-trade shock for now.”