Traders Plot Worst-Case Scenario for Yen If Crisis Hits

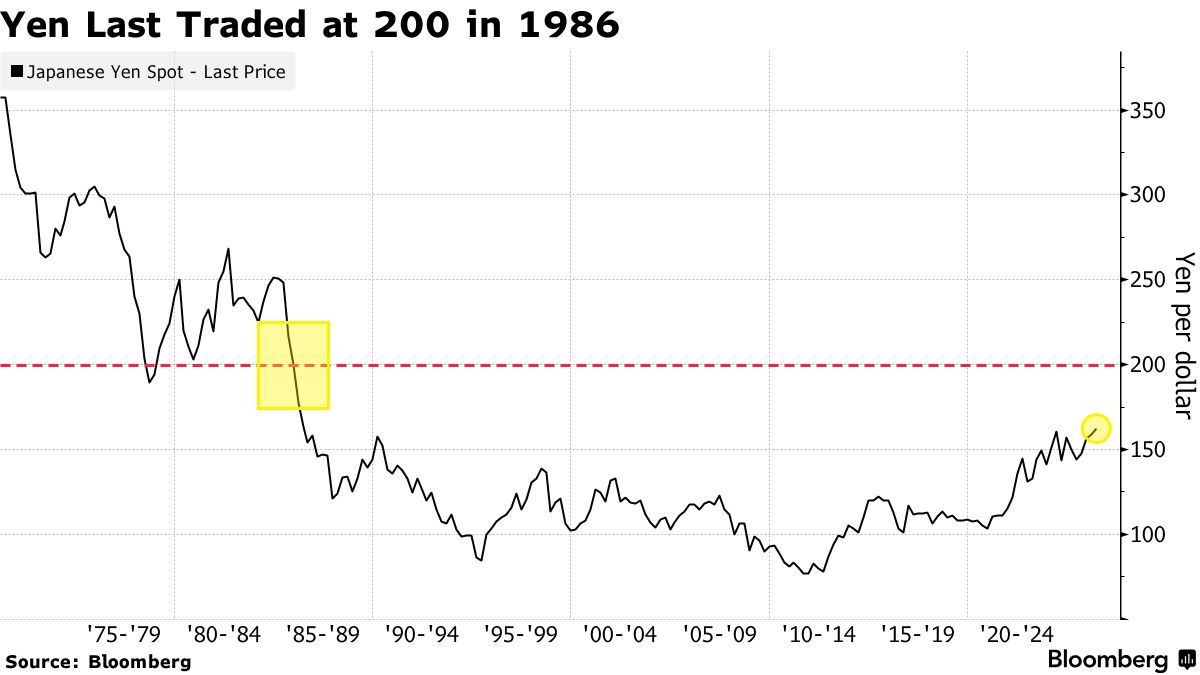

The yen sliding to a once-unthinkable 200 per dollar level is now a medium-term risk — albeit an extreme one — for some investors.

Under siege from Japan’s wide interest rate gap with other major economies and deepening concerns about Tokyo’s fiscal outlook, the yen has tumbled to a 1986 low and cemented its place as one of the worst-performing major currencies this past year.

Traders see little long-term relief from the Japanese government’s repeated warnings that it will take to stem the decline. Any official intervention to bolster the yen is seen by many as a mere speed bump as investors judge Japan to be a laggard in raising interest rates to combat inflation, underpinning its structural weakness.

T. Rowe Price, a money manager, sees the 169 per dollar mark as a potential worst-case scenario. Mizuho Bank draws the line at 170. Japan’s second-biggest bank Sumitomo Mitsui Financial Group Inc. mapped out in the coming years as one outcome.

Others, like Monex Group’s Jesper Koll and Calvin Yeoh at Blue Edge Advisors, consider 200 and beyond within the realm of possibility should the Bank of Japan fall further behind in tightening policy. The currency traded around 162.56 on Thursday morning in Tokyo.

“Without any intervention either directly in the currency or from the BOJ hiking, dollar-yen is threatening to look like my cholesterol — 180 to 205” by next December, said Yeoh, a portfolio manager at the hedge fund in Singapore.

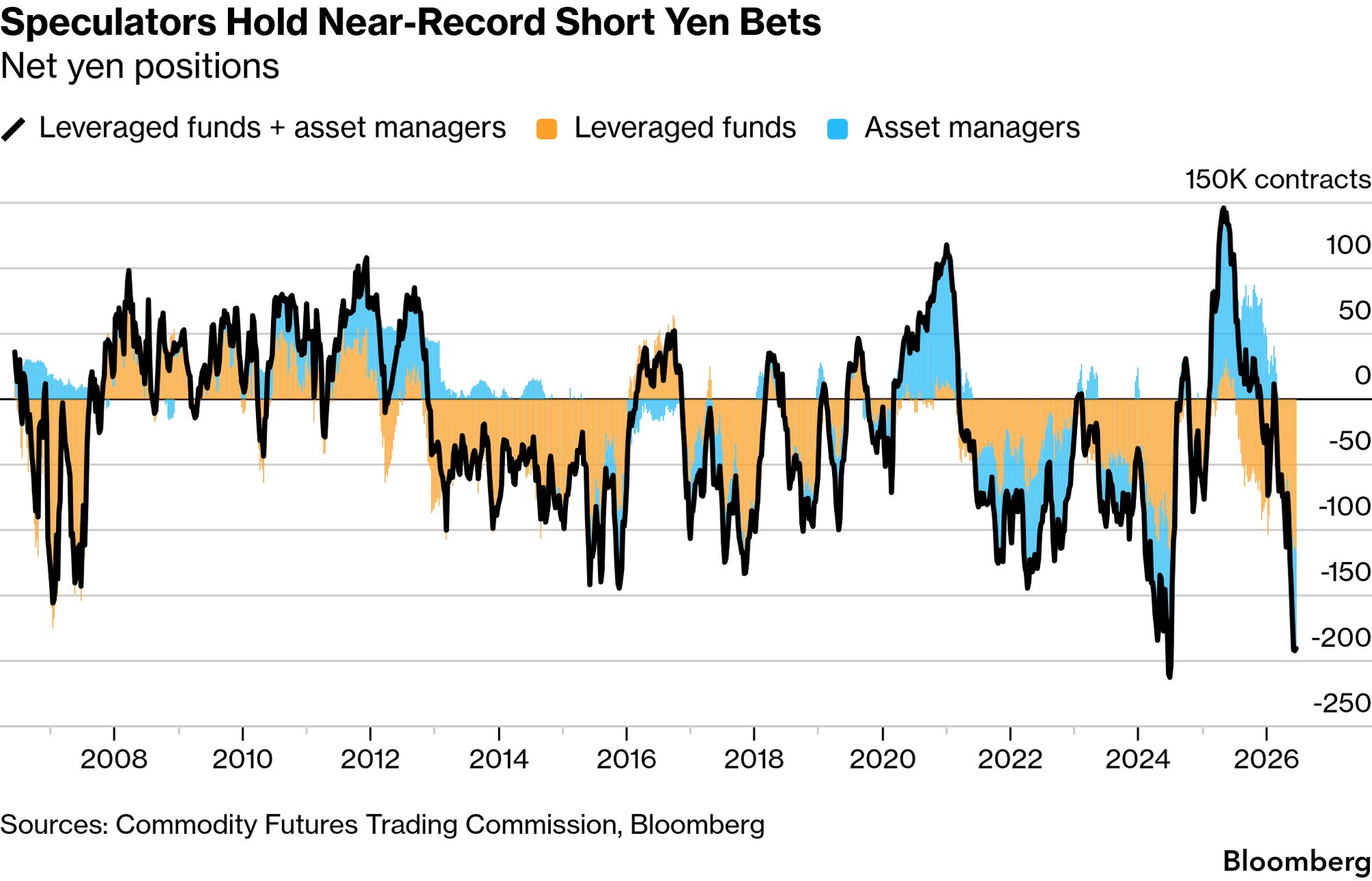

Positioning data supports the outlook for further yen declines.

Hedge funds ramped up their bearish bets on Japan’s currency last month to the most since 2017. Foreign-exchange options traders also point to risks of acute yen weakness, with about a 15% chance dollar-yen would rise to 180 in a year’s time. The possibility of 200 per dollar is still regarded as an extreme scenario in options markets, with such a case priced at less than 1% in the same time period.

To be sure, no one is saying a slide to 200 is imminent. To get there, the Federal Reserve would likely have to signal a more hawkish stance than markets anticipate in the face of re-accelerating inflation, thereby driving US Treasury yields sharply higher against those of Japanese government debt. Oil would have to skyrocket and geopolitical tensions take a turn for the worse.

Global sentiment would also need to deteriorate sufficiently to boost demand for dollars, according to asset manager Nuveen.

“The combination would likely also require the BOJ either delaying policy normalization or proving unwilling to push back against further yen weakness,” said Laura Cooper , London-based head of macro credit at the firm which oversees in assets.

The BOJ raised its benchmark interest rate by a quarter percentage point to 1% last month, the highest level since 1995 and signaled there would be more hikes. While that’s narrowed the gap with the US, some traders are that new Fed Chairman Kevin Warsh’s focus on price stability heralds higher rates. that the Japanese government wants the BOJ to go slow on further rate increases are fueling concerns over yen weakness.

“We are really at a cusp of a Japan currency crisis,” said Amir Anvarzadeh of Asymmetric Advisors, who has watched Japan’s markets for 37 years. “Much of it self inflicted by those BOJ policymakers who seem to be in a deep coma.”

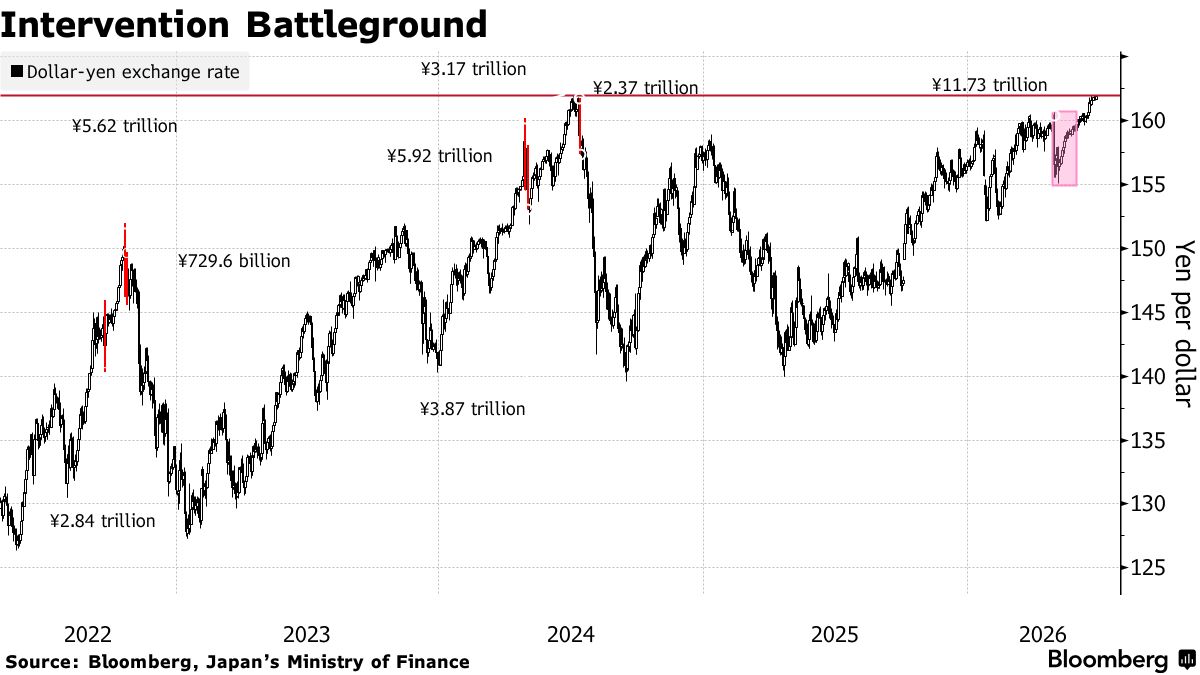

The Japanese government views its intervention earlier this year when the yen strengthened to about 155 per dollar as a success, Atsushi Mimura , Japan’s vice finance minister for international affairs, said in an with Bloomberg on Wednesday. The move had support from the US, he added.

But for now, yen bears are continuing to dominate the trading narrative.

Investors are focused on Japan’s heavy debt burden — which exceeds 200% of gross domestic product — and is the highest among major economies. Persistent budget deficits have raised concerns that Japan’s government is spending beyond its means. Mounting inflation stemming from the Iran war has also dented the yen, given Japan imports more than 95% of its oil from the Middle East.

“Japan’s macro, policy, and positioning backdrop still strongly favors a weaker yen,” said Ashwin Binwani , founder of Alpha Binwani Capital who has held bearish yen positions since the currency traded at around 155 per dollar. Being “short yen remains very attractive as long as those conditions persist.”

“The true worst-case scenario for the yen is not simply depreciation, but a disorderly one,” said Rinto Maruyama , senior FX and rates strategist at SMBC Nikko Securities. “Should FX intervention prove ineffective in such an environment, the market could begin to question the limits of intervention itself, further amplifying yen weakness.”

Then there’s the carry trade. A weak yen makes it a cheap source of funding to invest in higher yielding assets from the Turkish lira to stocks in India and Venezuelan bonds.

“Investors still love the yen to fund carry trades — even though yes, intervention risks are lurking,” said Nick Twidale of ATFX Global Markets in Sydney, who has traded the yen since 1998. His worst case scenario? “Absolutely in a year’s time, we could be at 200.”

Others are re-thinking their entire yen playbooks.

In London, Masayuki Nakajima , senior currency strategist at Mizuho, said there are “no technical levels” now for the yen.

Unless there’s a sudden weakness in the US economy or sharp drop in the dollar, “the 162 level should be viewed less as a ceiling and more as evidence of persistent structural yen depreciation pressures,” he said.

That’s spurring some investors to double down on their yen shorts, even at the risk of authorities dipping into their formidable in foreign currency reserves at any time to strengthen the beleaguered currency. Japan spent a record ¥11.73 trillion defending the yen from April 28 to May 27 after it first slid past 160 per dollar. Like the intervention campaigns in 2022 and 2024, however, this only provided temporary relief before the yen resumed its broader depreciation trend.

“Is there a red line at this point for Japanese authorities? I think at this point, there isn’t, quite frankly,” said Koll, an expert director at Monex, in a Bloomberg TV interview. “From a policy perspective, there’s a very clear recognition that, first and foremost, we’ve got to continue the path of expansive fiscal policy, plus only moderate increases in interest rates. So, for all intents and purposes, we’re going toward 200 yen.”