Colombia’s Tiger Trade Is Powered by High Rates, Fiscal Optimism

Investors are giving Colombia’s incoming president a vote of confidence, scooping up local assets on bets a rally will continue if he makes good on pledges to repair the country’s finances.

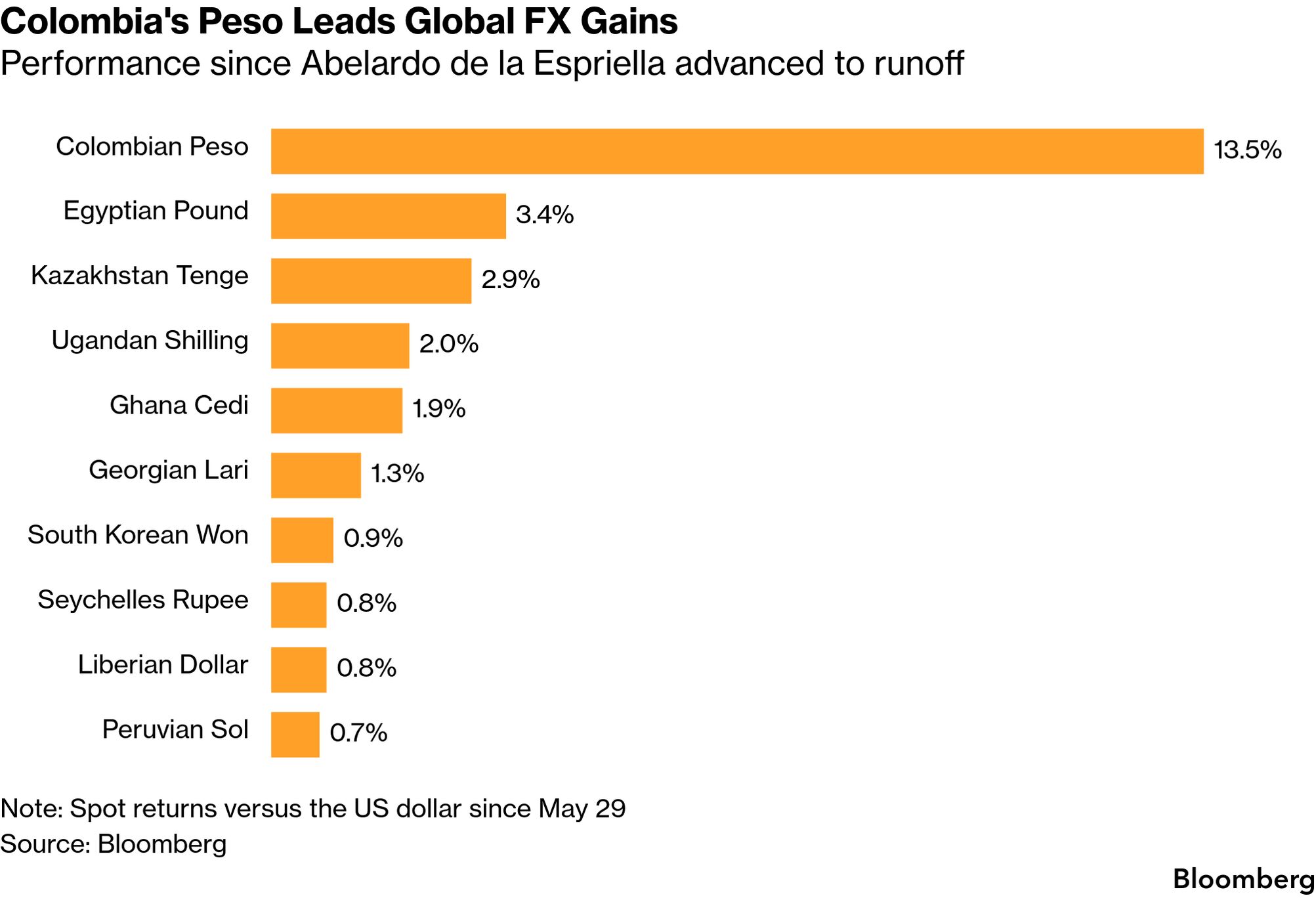

Local government debt has already nearly 10% — the best performance in Latin America — since late May, when Abelardo de la Espriella , a conservative outsider known as “The Tiger,” secured a spot in a runoff. Part of those gains are on the back of the peso, which is hovering near its strongest level against the dollar since 2019.

The Colombian currency has become highly favored among money managers this year. The Andean nation has some of the highest interest rates in the world, making it a popular option for carry trades. A hawkish central bank and high oil prices have further fueled the dynamic, sending the peso up almost 14% since De la Espriella advanced to the runoff, leading all other currencies.

“Among Latin America high-yielders, this is the one with the best story,” said David Austerweil , a deputy portfolio manager at VanEck. “Colombia sovereign credit spreads are the tightest they have been post-Covid, while local yields are still elevated even relative to recent history, so they are more attractive.”

The rally in local bonds marks a sharp shift in market expectations after four years under leftist President Gustavo Petro , whose administration left Colombia with one of its widest fiscal deficits outside periods of economic crisis. Mounting concerns over the country’s finances prompted S&P Global Ratings to downgrade the country’s credit score twice during Petro’s presidency, eroding investor confidence.

De la Espriella, who secured a narrow victory last month, has pledged to earn it back by tightening fiscal policy, cutting taxes and refinancing government debt. Jose Manuel Restrepo , his vice president, is in Washington this week to meet with multilateral lenders and the US State Department, a sign that the administration intends to move quickly on its economic agenda once it takes office on Aug. 7.

“We are positioned in local debt unhedged because we think the new administration has a credible target and both rates and the peso will benefit,” said Arif Joshi , a portfolio manager Bramshill Investments.

The president-elect has proposed slashing the size of the state by as much as 40% over his four year-term. That’s a positive sign for Joshi, who said that a plan focused on reducing expenses, rather than increasing revenue, is more legitimate.

Carry Play

Supported by high interest rates, the Colombian peso has become one of the best options for carry traders, who borrow in low-yielding currencies and invest in higher-yielding ones. The country’s central bank hiked its key rate by 75 basis points to 12% in June, further bolstering its carry appeal.

Pit against the dollar, the Colombian peso has yielded 22% from the carry trade this year, according to data compiled by Bloomberg. That’s the strongest return against the greenback by far.

Some analysts have raised questions about the currency’s longer-term prospects and whether De la Espriella, who won the election by just one percentage point, can garner the legislative support to enact radical change.

“We are skeptical he’ll be able to fulfill the high expectations,” Deutsche Bank AG strategists including Carlos Munoz Carcamo wrote in a note. “The market is pricing an overly optimistic view on Colombia.”

Still, most remain optimistic. JPMorgan Chase & Co. strategists upgraded their recommendation on the Colombian peso to overweight from a neutral position this week, saying that while a weaker-than-expected mandate could constrain De la Espriella’s agenda, early steps in the “right direction” should be sufficient to maintain market optimism.

“Positive sentiment is likely to be further supported by the central bank’s aggressive tightening cycle,” strategists including Tania Escobedo Jacob wrote in a note Tuesday. “This leaves Colombia offering one of the highest carry profiles in EM and should continue to provide support as long as broader risk appetite remains healthy.”