Inflation Fears Are Making Linkers a Winning Bond Trade in 2026

The last time oil prices spiked due to war in 2022, the rush to get protection with inflation-linked bonds . So far, this time is proving different.

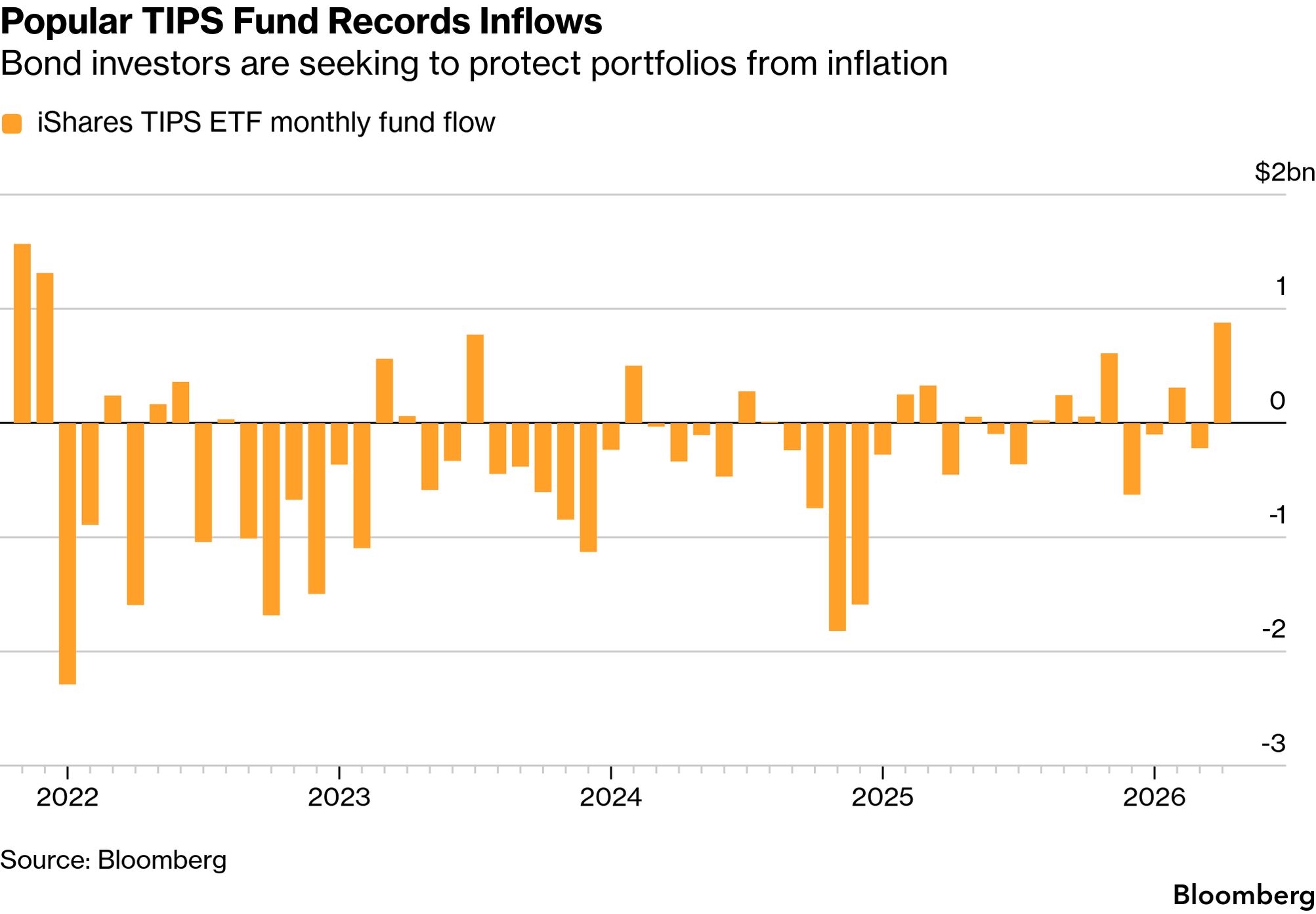

A gauge of global inflation-linked bonds is up 2% in 2026, ranking first out of the 24 key fixed-income indexes tracked by Bloomberg. The strategy is attracting a torrent of cash, with BlackRock Inc.’s $15 billion exchange-traded fund for US Treasury Inflation-Protected Securities pulling in its largest monthly inflows since 2021.

The bullish argument is that, even if energy prices continue to drop, the turmoil caused by the two-month war in Iran will have a lingering impact on the global economy. In the US, gasoline prices are near the highest since 2022, while in the Mideast damaged natural gas facilities may take years to fix.

While so-called linkers have a patchy history of protection — their value in 2022 when inflation surged following the war in Ukraine — those in favor argue it’s different this time around. RBC BlueBay Asset Management and BNP Paribas Asset Management are among those buying now.

“Inflation-linked bonds is a place you want to be hiding right now,” said Mark Dowding , chief investment officer at RBC BlueBay Asset Management. He sees value in such securities in the US, euro-area and Japan.

Inflation-linked bonds have often been seen as a staid investment, favored by the likes of pension funds seeking to match assets against their liabilities going out decades into the future. Yet when concerns about inflation grow, they can quickly attract a wider range of investors wagering on the direction of consumer prices.

Euro inflation-linked bond funds saw nearly €500 million ($588 million) in net inflows in March — the strongest since March 2022 — marking a reversal after almost a year of outflows, according to data from .

Breakevens Surge

The rush is showing up across market metrics. The extra compensation investors demand to hold US 10-year nominal bonds versus their inflation-protected counterparts — known as the breakeven rate — surged past 2.5 percentage points this week for the first time in three years.

A similar gauge in the euro area also hit the highest since 2023, and Japan’s equivalent has been testing 2% for the first time since the nation sold inflation-linked bonds over two decades ago. While oil prices are back at around $100 a barrel, that’s still up over a third since the war began.

“Stagflation risks are not fully priced in,” said Mohit Kumar , a strategist at Jefferies. “This scenario should see inflation-linked bonds performing as a protection from inflation moving higher.”

Linkers’ track record during inflation shocks isn’t straightforward. A potential shortcoming is that inflation-linked bond funds historically had a longer duration, meaning they were more exposed to changes in interest rates. That’s leading some investors to steer clear of them this time around.

“The clue is not in the title with the linker,” said Stephen Jones , global chief investment office at Aegon Asset Management. “The safety hedge that they supposedly offer an inflation shock is distorted and not delivered.”

Duration Problem

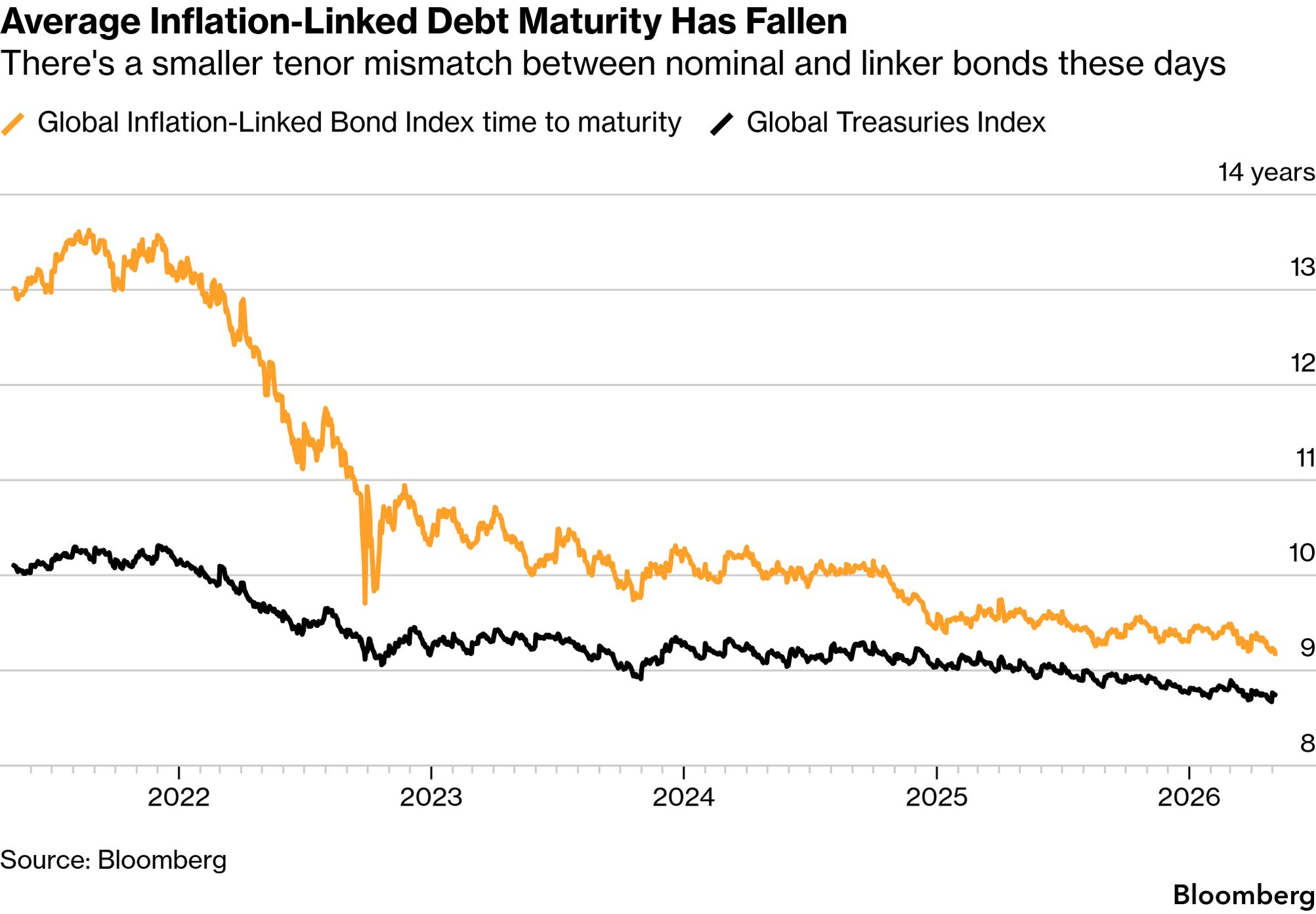

That’s been due to the fact that many governments tend to focus their linker issuance on longer tenors. In 2021, the Bloomberg global linker index had an average maturity of around 13.5 years, compared to about 10 years in a government bond benchmark. Their connection to inflation was then outweighed in the 2022 shock by their sensitivity to sharp interest-rate rises.

“This is not 2022,” said Elida Rhenals , senior portfolio manager at BNP Paribas Asset Management, adding linkers still have “super value.”

“This is only a supply shock — if there’s not a demand shock on it — real rates don’t have the room to increase as they did in 2022.”

Certainly, much has changed since then. Despite a recent cutting cycle by policy makers, interest rates are still much higher. And while major central banks are looking at precautionary rate hikes to combat the energy shock, so far they have held off to see how long conflict will last.

In any case, the average maturity of the inflation-linked index , in line with the government bond benchmark. And investors can always choose to invest in shorter-maturity linker funds or to hedge out the duration risk via derivatives.

Approaches that emphasize shorter-dated linker exposure and more targeted tools such as inflation swaps can enhance the hedging in bond portfolios, said Marc Seidner , chief investment officer for non-traditional strategies at Pacific Investment Management Co.

“People are underestimating the fact that you could have real growth and inflation accelerating at the same time,” said Adam Marden , co-portfolio manager of the Dynamic Global Bond Strategy at T. Rowe Price. “In that case, TIPS aren’t really gonna protect you.”

It might be better to play directly in the commodities driving inflation, according to Matthew Hornbach , global head of macro strategy at .

“Inflation-linked bonds by themselves are only a good inflation hedge relative to the nominal bonds. But they may not be outright a good inflation hedge,” Hornbach said.